How many add-ons is right for your car insurance?

This is a post for the savvy investors! the investors who really want to make their money work hard and enjoy the returns!! the newest financial product in the block!! and you must know about it!!

Are you a comfortable investor with diversity in mind? Have

done some investments in Equity, mutual funds, and fixed deposits? You will be

pleased to know that there are few more investment opportunities opening up your

way with some interesting #alternate-investment options.

One such concept I came across last week and wanted do a

basic research before sharing with you all. After checking online, I realised, the concept is globally recognised. The concept is peer to peer

lending. Globally a well-known concept, it is slowly but steadily catching up

in India, RBI has already published consultation paper on the same.

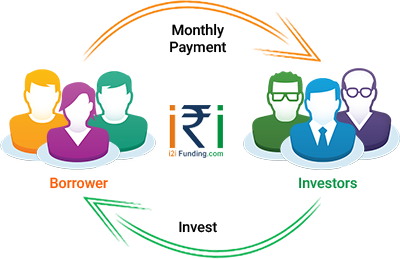

What is peer to peer

lending?

It is an easy concept of lending and borrowing, where the

investor and the borrower both are individuals and not institutions like Banks

or Non-banking finance companies. P2P lending in India concept thrives on high

income for investors on unsecured personal loans. #i2iFunding is one of the first movers in this space.These platform focuses on high vigilance and smooth interface.

How does it work for

the investors?

Investors need to do a simple registration on https://www.i2ifunding.com/.

- Registration - A simple form needs to filled including personal details

- Register as an Investor – Upload profession details, and upload address proof and PAN Card for verification purposes

- Review pre-approved loan projects – #i2iFunding only reflect the loan projects which ae pre-verified by the team basis the borrower profile and requirement. The loan request of the borrowers are verified by proprietary credit-score model and recommend interest rate

- Wallet - The investor can start investing from Rs. 5000 and multiple of 5000 upto Rs. 5 lakhs

- Physical verification and documentation – Once the loan approved by the borrower, i2i funding does a physical verification followed by signing a legal contract. Investor has to provide undated cheque equal to EMI amount for each investor. #I2ifunding shares the digital copy to each investor.

- Transfer funds and receive payments from next month – After all the legal formalities, investor needs to transfer funds directly to borrower’s account, and repayment starts next month onwards.

- Building a portfolio – Investors can give multiple loans and as per his risk appetite and earn monthly returns. ‘My Account’ section helps track investment details

Benefits for the investors-

- Diversify portfolio with high fixed income

- Freedom to chose loan projects based on risk apetite and return expectations

- Cap on funding each borrower at 20% of the loan amount, reducing over-exposure, concentration and mitigating risk

- Capital protection guarantee for the investors subject to the risk profiles of the borrower's of the loan projects (investing in loan projects of cat A borrower has highest protection)

Process for

Borrowers-

Once you are registered,

- Create a borrower account – Register with your personal details, income detail, employment status etc

- Loan assessment by i2i – 40 parameters including education background, CIBIL Score

- Make loan live on i2i funding website – Post the assessment, make your loan live on i2i platform

- Get funding commitment from Investors – Registered invetors across India can see your requirement and apply

- Physical verification and documentation - i2ifunding will do verification of original documents, you also have to share 3 EMI cheques for investors to hand over

- Loan disbursal and repayment – Once the verification done, lenders will directly transfer the money in borrower’s account and borrower need to start repaying from next month

Benefits for the

borrower

- Low Interest rates

- Quick hassle free process

- No pre-payment penalty

- Funding in few days

Charges you need to keep in mind -

Charges

|

Investor

|

Borrower

|

||||||||||||||

Registration

|

Nil

|

Nil

|

||||||||||||||

Create a borrower account

|

N/A

|

Rs 100

|

||||||||||||||

Create an investor account

|

Rs 500

|

N/A

|

||||||||||||||

Increase in the wallet

|

- Nil up to first Rs 50,000

- 1% for additional increase

|

N/A

|

||||||||||||||

For Salaried Borrowers

Loan processing fee payable before physical

verification. (Minimum processing fee is Rs 2000)

|

-

|

|

For Self employed

Borrowers

Loan processing fee payable before physical

verification. (Minimum processing fee is Rs 2000)

|

|

Other Charges

Investor

|

Borrower

|

|

In case of prepayment

|

-

|

No Charge

|

In case of change in loan amount before receiving any funding

commitment post listing

|

-

|

Rs 100

|

In case of change of bank account details

|

Rs 200

|

Rs 200

|

My take - It is an interesting #alternate-investment option, with stringent guidelines. However, it is new in India. Investors with moderate to high risk appetite can look at it. One may look at borrowers with high ratings like A-D for good yet safe return on investments.

Checkout the website https://www.i2ifunding.com/ for partnership program too!!